uʍop ǝpısdn

Risk-free rates are costing the US government sector a not-at-all-pretty penny

The distortions in the US plumbing continue to throw up such perversity that it’s hard to look away. The recent decline in ONRRP is a case in point. The decline in money market holdings at the Fed serves to highlight the not-insignificant cost of recent policy, which is now partially transferred from one part of government (the Fed) to another (Treasury). It certainly isn’t boring, but it is also kind of uʍop ǝpısdn for assets deemed the lowest risk in the entire world.

Those with long memories may recall that Raphael Bostic, the Atlanta Fed governor, in January 2022 told us the Fed should reduce its balance sheet aggressively. The Fed had plans quickly to pull “at least $1.5 trillion” out of financial markets that Mr Bostic considered pure "excess liquidity." That figure more-or-less matched the total parked in the ONRRP at the time ($1.65 trillion). Some (me) took his comments to mean the Fed anticipated a straightforward balance sheet reduction, with a fall in ONRRP of the same magnitude, without touching sensitive banking liquidity of reserve balances.

I had my doubts at the time. Turns out Mr Bostic, or those who advised him, vastly underestimated the attractions to money-market funds of ONRRP. With an acutely inverted yield curve and rates on a steep upward trajectory, ONRRP remained a stubbornly attractive investment. Conventional wisdom was turned upside down. It may be weird, but the result is a logical consequence of massive COVID-era QE, followed by the inevitable leap to higher interest rates to fight resulting inflation.

Eighteen months later the Fed’s balance sheet is only ~$570 billion smaller and until recently, all of the decline in liabilities has come from government and bank holdings at the Fed, not money market funds. I suspect the earlier optimism of balance sheet adjustment reflected a widely held Fed view of how the plumbing should be arranged, rather than how it had re-arranged itself in response to Fed policy.

Not surprising, then, there is detectable joy in the ‘delayed gratification’ of recent sharp falls in ONRRP. Some, like Joseph Wang (@FedGuy12) today celebrate the huge T.Bill issuance that successfully, and more-or-less equally, drained the ONRRP ‘enabling an extended QT’. That’s a fair point, but may underplay the cost.

The failure of the ONRRP to decline ‘organically’ as expected, means the federal government has had to ‘buy’ the reduction by paying a considerable premium on T.Bill rates. The reduction in cost to the Fed the decline in ONRRP represents, actually means the consolidated Federal government is paying MORE than would have been incurred had the ONRRP balances remained unchanged.

I looked at this briefly before, and its worth another look, because the sums involved are not trivial. The $2 trillion of T.Bill issuance in the last month or so is way higher than the normal $1.3 trillion average monthly issuance. And average rates are higher too.

ONRRP rates since the Debt Ceiling settlement have remained at 5.05%, meaning the US Treasury has had to pay between 13 and 37 basis points extra to entice funds into T.Bills and out of the Fed. That amounts to an additional cost to the US tax payer of approximately $1.5 billion so far since settlement of the Debt Ceiling. If more balances are transferred from ONRRP the cost will rise.

Short-term T.Bill rates currently deliver the highest rates on the Treasury curve by some distance, and the highest T.Bills rates since the year 2000. So, the issuance of such high T.Bill volumes leaves something to be desired as a portfolio management decision.

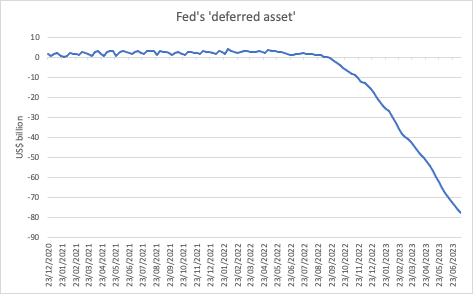

The additional T.Bill cost is dwarfed by the current annualised cost to the Fed of the ONRRP, which amounts to over $100 billion (~$2 trillion at 5.05%), or ~$275 billion if the cost of Interest on bank reserves (IOR) is taken into account. That cost goes a good way to explaining why the Fed is currently running a loss (or, ‘deferred asset’ as they prefer to call it) of $78 billion; a figure that promises to grow significantly in coming months, even if the ONRRP continues to fall.

Which just goes to show that, whether the cost falls on the Fed, or is paid for by the Treasury through higher T.Bill rates, a considerable drag on consolidated government resources has to be paid - to banks and money-market funds - for past policy. That this colossal extra cost is now deemed necessary also reflects a permanent fiscal enlargement that central bank and Treasury have opted for. You don’t get something for nothing.

It’s not boring, but it is ʇuoɹɟ oʇ ʞɔɐq puɐ uʍop ǝpısdn.

That's ongoing stealth QE as well? No wonder the risk assets are still strong.