Puzzling Issues

ONRRP, T.Bills and repo clogging FedWire - will we need more reserves soon?

I was briefly traumatised during Lockdown by a failed attempt to complete a jigsaw of van Gogh’s Almond Blossom. It looked straightforward, but it wasn’t, at least for me. After two weeks, suffering recurrent swimming visions of blue, I gave up. My wife completed it.

This post is a dive into the puzzle of US liquidity following the Debt Ceiling settlement. It looks at T.Bill issuance, short-term interest rates, repo and the changing allocations of various players and the settlement system. Much less confusing than van Gogh, though with a few distinct wrinkles.

Why is this important? Because market structure at the short end has a direct bearing on the operational stability of the US banking system, and therefore for markets everywhere. And a real puzzle may be emerging over the capacity of the Real Time Gross Settlement System known as FedWire.

The US Debt Ceiling agreement was reached on Friday, 2nd June, and signed into law the following day. Treasury Bill issuance began in earnest the following week with a total of US$ 701 billion issued since at an average rate of about 5.26%.

Any rebuild of the Treasury General Account is a net drain of liquidity from the system. However, it makes a difference whether the drain comes from money-market funds lodged in the ONRRP, or from the banking system via system reserves. So far, paying a high yield to money-market funds has protected system liquidity.

All the T.Bills issued in June have been considerably above ONRRP rates. In fact, longer dated T.Bills came at a significant yield enhancement even to the equivalent SOFR term rates. Admittedly, this is a perilous calculation as the timings cannot be certain and forward SOFR daily ranges averaged 7-10bps so far in June.

Nonetheless, it’s pretty clear money-market funds needed a lot of extra return to buy T.Bills. It seems to be working. As at Friday 23rd June, the money-market holdings in ONRRP fell by $285 billion since 2nd June, while the Treasury General Account (TGA) rose by US$ 329 billion. It is likely the high issuance and higher Bill rates helped drive up forward SOFR rates since the beginning of the month.

As long as T.Bills offer a premium to ONRRP, money-market funds will tend to favour switching out of ONRRP and into T.Bills. This allows the Reserve Balances of commercial banks at the Fed to remain stable around US$ 3.2 trillion. Internal calculations at the Fed suggest a ‘safe’ lower bound for reserves is around US$ 3 trillion, though this may have declined a little as deposits continue to fall and banks seem to operate some kind of informal ‘reserve requirement’ against their deposits.

Keeping the T.Bills elevated relative to ONRRP (and thus maintaining the liquidity safety margin) is expensive. So far, I estimate the extra ~20bps paid by T.Bills over ONRRP has cost the Treasury US$1.4 billion dollars since the beginning of June. Assuming Treasury and Fed continue to see eye-to-eye on a shift from ONRRP to T.Bill investment, the Treasury are going to have to keep paying. It is going to be a hefty bill if the target level of USR 800 billion in the TGA is to be met.

So, policy makers also need to ensure the liquidity drain of the TGA continues to flow from the ONRRP. Money market funds have tended to increase ONRRP holdings at quarter-end. In the face of continued Treasury issuance, a preference for ONRRP by money-market funds would deplete system reserves and shift system liquidity towards the anticipated lower bound. If that were to happen, repo rates may spike and liquidity for the entire system may become constrained.

Yes, the Fed has initiated a Standing Repurchase Facility to cap funding rates if liquidity become short. It may help but it’s another ad hoc solution to add to the financial plumbing since the GFC.

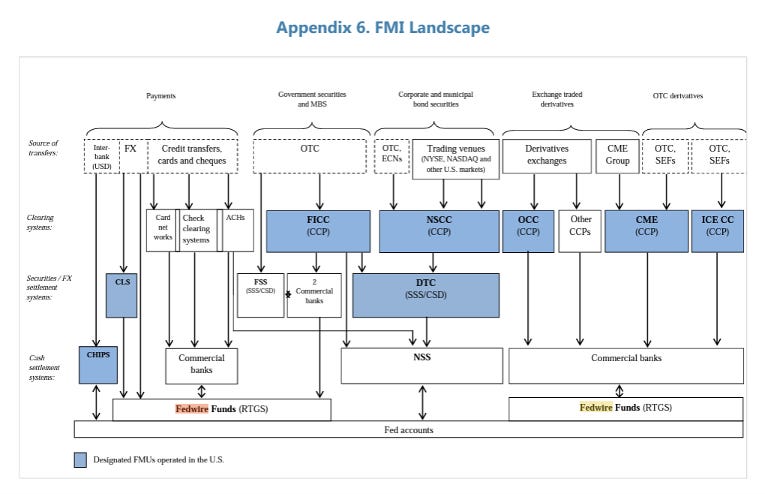

Then there is a puzzle yet to be explained. The very large amounts of repo being transacted every day due to ONRRP is hogging FedWire capacity. FedWire is used to settle all manner of financial transactions, as this graphic from a 2020 IMF paper makes clear.

According to SIFMA figures, daily turnover of FedWire eligible Tri-party repo has recently exceeded daily turnover of FedWire itself for the first time ever. The bulk of the turnover coming from money-market funds placing collateral with the Fed in ONRRP.

The main dollar Real-Time Gross Settlement system is now pretty much dedicated to overnight repo transactions. How this affects other parts of the financial system is not entirely clear. Settlement of other transactions can be made via other channels, but all dollar balances between banks settle through Fed in the end, and FedWire is the normal conduit.

Velocity of FedWire transactions may need to increase, or the stock of reserves held by commercial banks may need to increase again at some point. And an increase in stock of reserves may mean an expansion of the Fed’s balance sheet - as happened in early March. This FedWire congestion puzzle remains. I haven’t got an answer for it. Solutions gratefully received.

My experience is that when flows become excessive, problems don't occur immediately, but gradually build in a manner where things seem fine until they are not. I suspect there will be another hiccup of some sort that will be glossed over by the Fed, but actually be important.