Speculating about speculators

Money market allocations, bond/futures basis and ONRRP - not boring, really

Recent investment flows at the very front-end of the Treasury market have a couple of discrepancies. So far, so boring, you say. Well, perhaps not boring. Discrepancies raise interesting questions. One question may be: “are these flows related to the financial stability concerns expressed by the Fed and the BIS among others?” Specifically, do discrepancies relate to a perceived risk in bond/futures relative value trades? They may do. Which may influence how we think about recent changes in ONRRP holdings at the Fed.

Data published by the Investment Company Institute shows government money-market funds increased their assets under management by nearly $200 bln (actually $193 bln) in the third quarter. During the same period, funds increased their holdings of Treasury securities by $461 billion. How is that possible? That is Discrepancy One.

Well, the same ICI report also shows money-market funds reduced repurchase agreements (repo) on Treasuries by $306 bln in the quarter to a total of $1.9 trln. This is Discrepancy Two. Because despite this fall in repurchase agreements, the ‘stock’ of reported repo transacted by money-market funds is now larger than the total outstanding repo in the Fed’s ONRRP ($1.56 tln at the end of the quarter). By inference, money-market funds must have increased repo transactions with counterparties other than the Fed, even though their overall commitments in repo have declined.

There are an obvious set of borrowers from money market funds who may account for Discrepancy Two. Namely hedge funds engaged in the cash/futures basis trade in Treasury market which have given the Fed and the BIS cause for concern.

I won’t rehearse the mechanics of the basis trade here. A very good article has been written by Daniel H. Nielson last week, using clear T-accounts to illustrate the transfers of assets and liabilities. You can read his explanation here:

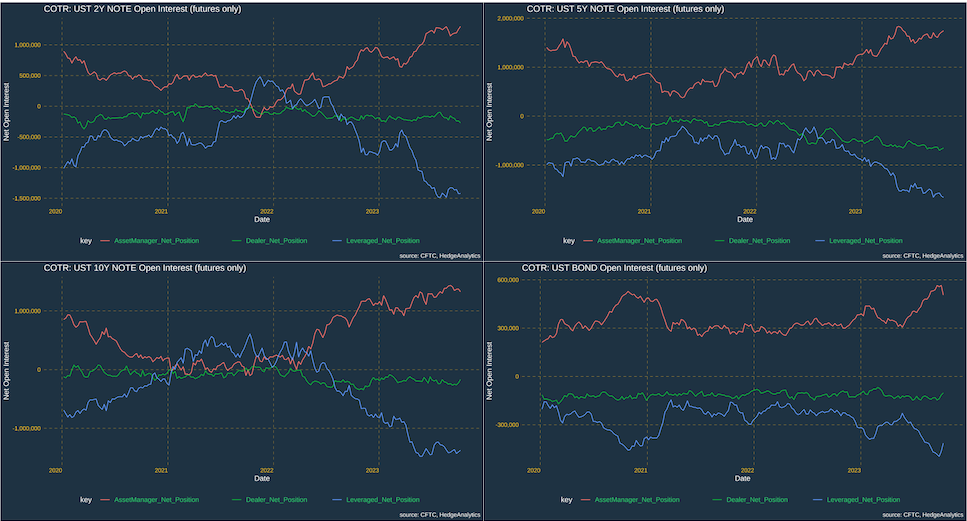

My interest is how the basis trade may link to money-market fund behaviour. Coincidence is not causality. But there is some suggestive correlations between the shift by money-markets funds into repo facing non-Fed counterparts and changes in futures Open Interest.

The basis trade can be seen in reported futures Open Interest when hedge funds, who specialise in cash/futures basis, adjust their net short futures as they seek to profit from rich futures/cheap bonds. Part of the trade requires cash borrowed in repo to buy the cheap bonds. The futures/bonds spread has recently been elevated and hedge funds have been taking advantage, reflected in a rise in net short Open Interest by ‘Leveraged’ accounts in all Treasury futures contracts, especially from March to May 2023 onwards - as the blue lines show in the charts below.

The latest moves down in blue lines kind of (not exactly) coincide with the rise in lending of cash by money-market funds to non-Fed counterparties in Treasury repo which became evident from May onwards.

It looks as if one of the reasons the ONRRP facility has declined sharply in recent months may be because of the attractive returns offered by hedge funds borrowing cash to buy Treasuries for the basis trade.

Whether you read Daniel’s explanation or not a major point to grasp is that the cost of funding is a key variable in the profitability of the basis trade. Repo rates tend to rise at quarter-end periods, at least since late-2022. Mostly, repo falls again after quarter-end. However, after the end of the third quarter at the end of September, repo rates have remained high, especially GCF, as the following chart shows (inspired by an earlier Daniel H. Nielson study). This may be hurting the cash borrow side of the basis trade, although the nature of the trade means offsetting profits from the fall in bond prices means the trade is probably overall profitable.

I had assumed the upward pressure on repo was due mainly to the large issuance of T.Bills following the resolution of the Debt Ceiling dispute. The higher repo rates reflected the higher rates required by T.Bills to rebuild the TGA.

But as the funds under management in money-market funds has increased , it seems hedge funds may be competing with T.Bills issuance to absorb the new money. The basis trade may also add upward pressure on repo rates.

Why is this worth rehashing? Well, regulators are concerned enough to air their worries. The BIS reported that ‘speculative positions in US Treasury futures… have been concentrated in the belly of the curve'. This is true in terms of face value, but as I recently pointed out, it is dollar risk per basis point (DV01) which is the true measure of risk in bond markets. Adjusting for DV01 shows the risk is spread pretty evenly across the curve - assuming I’ve divided by the right number of 000s!

Is this worrying? Not necessarily. As I said, the higher repo costs are probably offset by gains from the convexity of the trade - it acts like a cheap option on bond yields. This may change if repo shoots up, or margin calls are raised significantly on futures forcing some accounts to exit the trade.

It is also interesting that the fall in ONRRP holding at the Fed may be related to the rise in the bond/futures basis trade.

It certainly shows that discrepancies can lead to some interesting speculation, in this case about speculators.

“the nature of the trade means offsetting profits from the fall in bond prices means the trade is probably overall profitable…. the convexity of the trade - it acts like a cheap option on bond yields.” - do you mind elaborating on this ? Much appreciated

My wonder is why there is a consistent arbitrage between futures and spot Treasuries, you would imagine that with so much pressure from HF it will go down. Any idea?