The Crack Up

Pessimism in Treasuries

“By God, if I ever cracked, I'd try to make the world crack with me.” F. Scott Fitzgerald in ‘The Crack Up’, a 1936 collection of essays by F. Scott Fitzgerald in which he grapples with despair after the heady years of the Jazz Age.

What ails the bond market? Simply put, rather unexpectedly, yields across the curve are moving higher. During the last few days it sometimes seemed yields were, like occasional tech stocks, ‘melting higher’. There are two proximate causes for the bond market’s problems. The first is that this week’s FOMC ‘dot plot’ pointed to ‘higher rates for longer’. The expected funding cost of holding bonds just became more negative for a longer period. The second is the dawning realisation we have moved well past any benign environment for Treasury issuance. The Treasury General Account is restocked which means new money borrowed will turn increasingly to coupon issuance, rather than T.Bills. With that comes the threat of a distinct turn upwards in the duration cycle of the bond market. Duration is volatility in disguise. Quantitative easing attempted to remove duration, and therefore risk, from financial markets in an attempt to persuade investors to boost asset prices. Now we are facing a long-term rise in duration entering financial markets. And on top of that, market structure forced on dealers in the aftermath of the GFC mean the Treasury market is less resilient to volatility.

This week’s FOMC outcome (and the accompanying economic/monetary projections) cannot have been a huge surprise. The outcome was a close reflection of the Beige Book outlook published a couple of weeks ago. Its publication led me to suggest that the Fed would conclude ‘a/ ‘inflation’ is not yet sufficiently subdued, and b/ reduced concern about a weakening economy’. And so it transpired.

Of course, the bond market is concerned by higher for longer cost of funding. But it is the dawning realisation that investment risk has become skewed higher; a combination of negative carry, liquidity constraints and anticipation of a deluge of coupon issuance. None of this is appealing for investors - or dealers, for that matter.

Everyone knows the deficit is not where it should be given the still-high level of employment and the continued robust growth of the US economy. If there actually is a recession to reduce government receipts and increase outlays, Heaven knows where it will be. But even if no recession appears, the Treasury has largely replenished its cash holdings through T.Bill issuance (at high cost). In future, debt finance will swing back to coupon issuance.

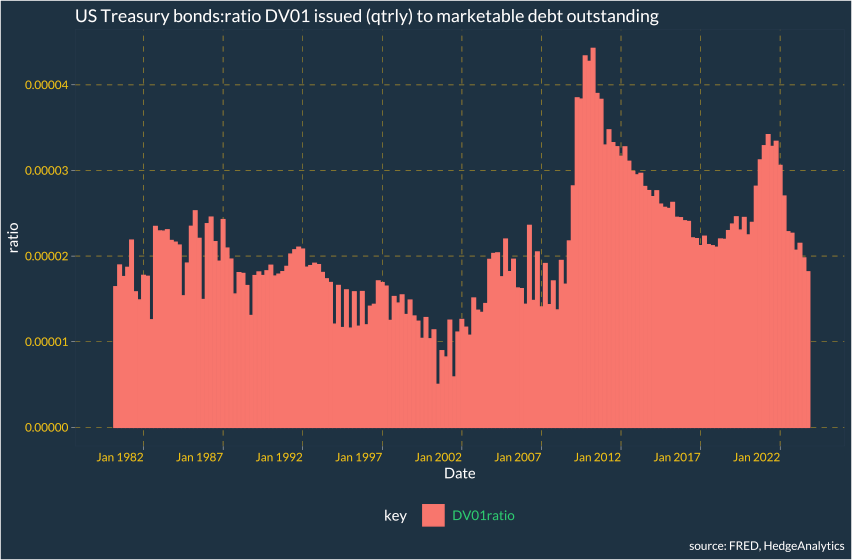

One way to visualise this is the ratio of dollar value of a basis point (DV01) issued by Treasury each quarter to the outstanding marketable debt. Using data back to 1979, this ratio spiked in the GFC and in the COVID19 pandemic, but in both cases was offset by Quantitative Easing, where the Fed offset some (not all) of this extra price risk plus signalled prolonged low interest rates. The combination worked well to stabilise the demand for bonds.

At the end of September, the ratio is likely to be the lowest since Q2 2008. This has been achieved, despite the very large public deficit, because funding has been skewed towards the short-end (including Bills). This fall in the ‘duration cycle’ is surely at or close to its low. Only during the late-1990s era has it been substantially lower. That was a time when investors worried about the disappearance of Treasury issuance due to repeated government surpluses. That is certainly not a credible concern now. With the cash position of the government rebuilt, accelerating future issuance is likely to swing back towards longer-dated bonds, pushing this ratio higher, this time without the backstop of Fed buying.

But don’t take my word for it. Here is a quote from Assistant Secretary for Financial Markets at the US Treasury, Josh Frost speaking on 21st September (yesterday):

“While bill supply is likely to remain above 20 percent for some time, our intention is to gradually increase coupon issuance to better align auction sizes with intermediate- to long-term borrowing needs, and as I outlined at the August refunding, we expect that further gradual increases in coupon auctions sizes will likely be necessary in future quarters.”

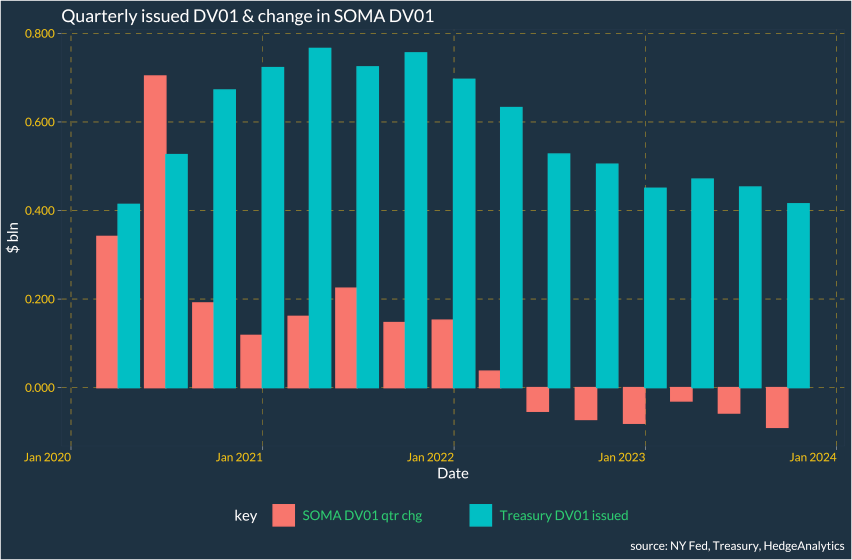

The first six months of 2020 saw the Fed absorb more DV01 with its System Open Market Account (SOMA) than was issued by the Treasury - at least according to my calculations. The Fed continued to help out as issuance ramped up to end-2022. It was part of a multi-pronged approach to ensure Treasury markets behaved, after nearly collapsing in March 2020. But those days of Fed support are gone.

That’s not to say the Fed QT is actively depressing bond prices. The reduction in Fed portfolio delivers very little extra DV01 into the wider investor base. This is not the reason for a turn in the duration cycle. As Fed portfolio bond holdings are reduced by redemption, the decline in DV01 of the remaining portfolio is a slow process - a redeeming bond has negligible DV01 and in any case, portfolio management concerns force the Fed to extend maturities every quarter.

But we don’t need QT to be worried about bond market volatility. There is distinct nervousness about the resilience of the Treasury market from several quarters.

For instance, dealer capacity is falling relative to outstanding Treasury bonds. The following chart showing the ratio of outstanding Treasury debt to Total Primary Dealer balance sheet size makes that stark point. It is taken from an important paper by Darrell Duffie presented at the recent Jackson Hole seminar.

The fear about Treasury market resilience is also present in recent papers on the Treasury bond basis trade - by both the Fed and just this week by the Bank for International Settlements. Both papers worried about the impact such trades may have on the proper functioning of the bond market.

The theme made a reappearance just yesterday with an ISDA sponsored conference, which was attended by senior Treasury officials entitled ‘The Path to Resilient Treasury Markets’.

The cost of funding (Fed Funds) is important, an inverted yield curve, liquidity concerns all act as an inhibitor to bond investment. That may change when it is clear that rates are headed down. But above all right now a bigger problem is the stream of duration risk that threatens the market, with a rising concern that liquidity may not be quite as robust as has been assumed.

Towards the conclusion of ‘The Crack Up’, Fitzgerald expresses pessimism for his, and America’s future: “I think that my happiness, or talent for self-delusion or what you will, was an exception. It was not the natural thing but the unnatural—unnatural as the Boom; and my recent experience parallels the wave of despair that swept the nation when the Boom was over.”

“Duration is volatility in disguise”

Great article. One question: in your first chart, is the denominator for the ratio the dv01 or notional amount of outstanding debt? The former seems the right measure to me, but wanted to double check?