Homeward Bound?

US banks restrict funds for financial assets, and turn instead to loans

Liquidity regulations put in place after the GFC are now clearly constricting financial activity and driving banks back towards traditional income sources. Very bad for global financial assets, but possibly not so bad for the US economy.

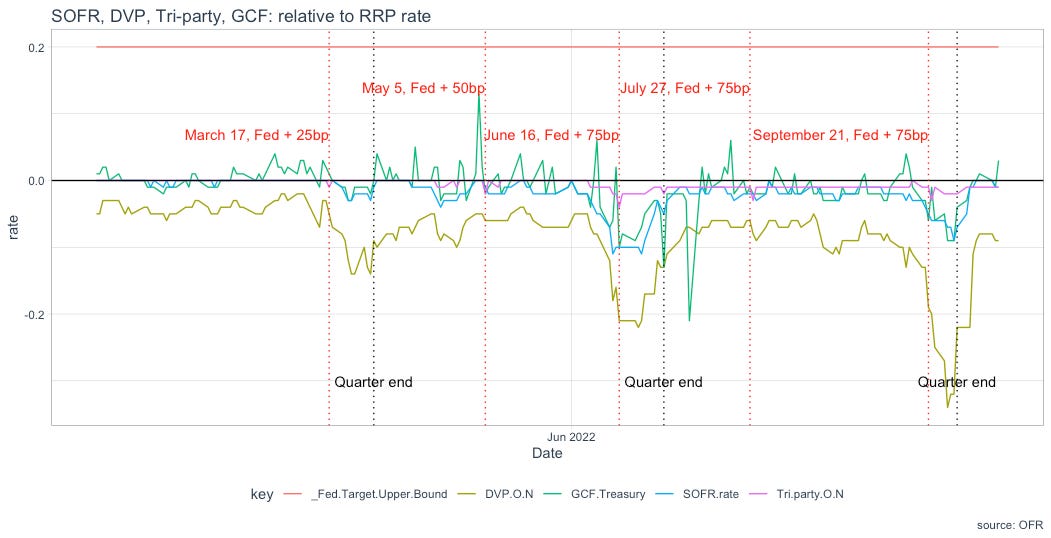

The following chart shows various US repo series against RRP rate (denoted as 0 horizontal line), i.e. the chart abstracts repo behaviour from the level of rates. Clearly, repo is responding NOT to Fed rate rises but to quarter-end restrictions banks impose on their balance sheets.

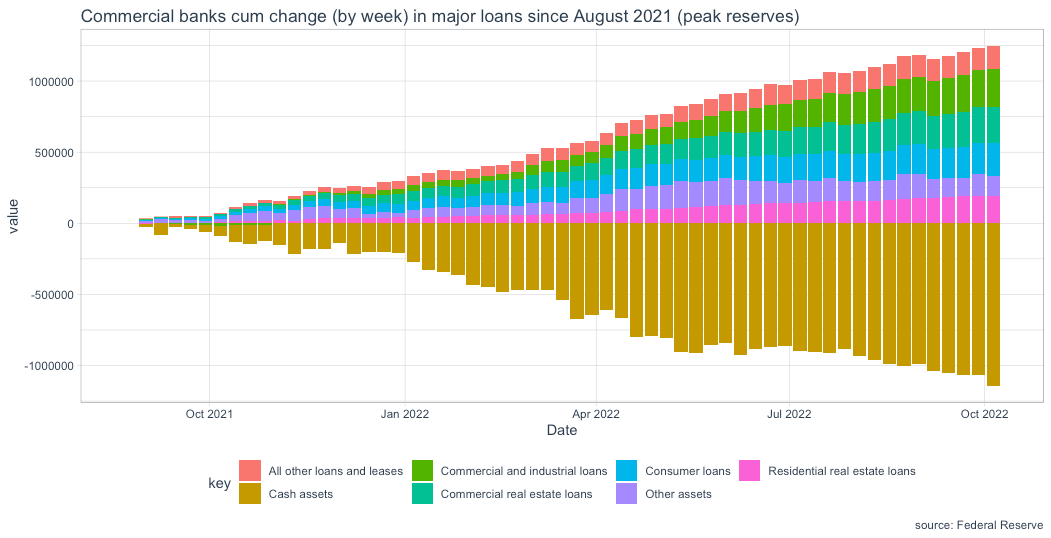

Yet, US banks are expanding loan books almost lock step in the decline in cash holdings (reserves) which reflect Fed tightening. Banks are moving back towards traditional sources of income. Very bad for global financial assets, not necessarily bad for the US economy.

I'm sure this is a bad question but why would "US banks are expanding loan books almost lock step in the decline in cash holdings (reserves)" reflect Fed tightening? Wouldn't US banks make less loans as rates go up?

Thanks for pointing this out Meyrick. Traditionally the quarter end turn coincided with extra demand for funding ie Q3 2019. That no longer seems to be the case, at least in 2022. Do you think that’s a result of still being in an excess reserve position or a result of the changing nature of bank exposures as you highlight in your post? Thanks