Short-Term Parking

How not to fix the US’ fiscal problem

United States government finances are in a dire state and getting worse. The Congressional Budget Office (CBO) says so, the IMF says so, the investment community say so. The gold price is saying so. The average annual fiscal deficit for the term of the Biden administration was more than 7% of GDP – the latest CBO estimates suggest the current year will show a deficit of 6.7% of GDP. No real improvement is expected in future years, which will leave the stock of government debt at 122% of GDP in 10 years’ time, according to the CBO. Sadly, this estimate is likely to underestimate the actual deterioration. Usually, denying difficult reality makes matters worse. But denying reality may be what Treasury has attempted to do through a strategic rejig of the maturity profile of US Federal debt. The ploy almost certainly added future costs and risks in the Treasury market, borne by future US taxpayers. It may also add to future instability in the Treasury market itself.

The Treasury strategy were spelled out in a paper in July 2024 which dubbed the practice ‘Activist Treasury issuance’ (ATI). Radical market changes dictated by post-GFC regulations created the conditions for its development; an example of unintended consequences of financial ‘reform’. There may have been short-term, presentational benefits to the Biden administration. The downside is higher current cost and painful remediation by future Treasury officials.

ATI mirrors the Fed’s Quantitative Easing (QE) program. The Fed’s QE exchanged investors’ fixed coupon long-dated debt for floating rate debt. QE took long duration risk away from investors and added short term interest rate risk. The aim was a) to reduce long-term borrowing costs and b) force the investment community to invest less in Treasuries and more in iskier assets such as shares, in the hope of boosting economic growth, a practice given the inauthentically academic title of ‘portfolio rebalance’ by the central bank.

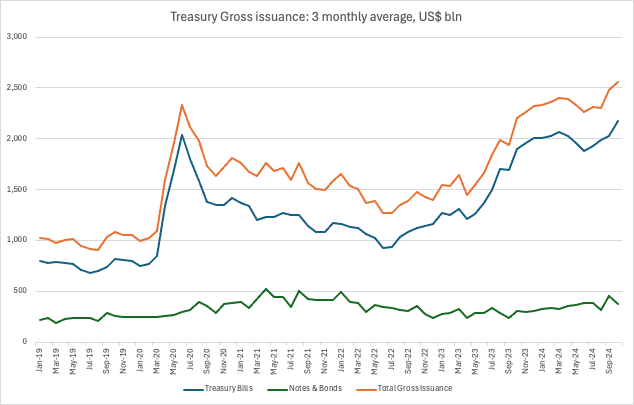

Treasury has followed a similar strategy. In the last 2.5 years Treasury issued an additional $1 trillion T. Bills (floating rate debt) and simultaneously contained Treasury Note issuance with maturities of 2-10 years. The July paper concluded this switch caused 10-year yields to be up to half a percent lower than otherwise.

The Treasury strategy neatly dovetailed with the reversal of the Federal Reserve’s QE holdings. Treasury Bills outstanding increased as Fed liabilities declined in broadly similar fashion. So, short-term interest rate risk was transferred from Fed to Treasury. Short term debt has less stable interest costs and needs to be re-issued more often. The danger of sudden slip-up with catastrophic consequences is higher. Concentrated short-term interest rate risk is dangerous. It is what caused the Global Financial Crisis in 2008. Just because the issuer is the US Treasury does not make everything safe. The Fed can control short term rates and risk, the Treasury cannot, unless it overtly interferes with central bank policy. Without assured low short-term interest rates the Treasury’s maturity switch will only add to interest costs and funding volatility. Not only did ATI add to interest costs; the strategy looks like it will add complications and further costs for a future Treasury Secretary.

What benefits the Treasury could see from concentrating so much debt issuance at the least attractive part of the yield curve for issuers? Two main drivers:

1)Investor demand for money market funds as Fed rates rose drove demand for short-term instruments. Defenders of the Treasury program claim simply to have responded to increased demand created by growth of money-market funds. But here’s the thing; Treasury Bills sold by the Treasury were reliably offered at higher interest rates than those available on Fed instruments. That suggests the Treasury actively sought to persuade take up of its paper. This is evidence of conscious promotion of short-term funding by Treasury.

2) The precarious fiscal position raised Treasury concern that issuance would damage the 10-year benchmark further. The 10-year yield is the benchmark of the health of US government debt. Increasing short-term instruments helped reduce issuance and contain yields in the 10-year sector. This was an illusion. Short-rates are higher than 10-year rates; overall interest costs increased even if it helped 10-year yields in the short term.

There is a sting in the tail for an incoming administration. If the monetary cycle has peaked, as recent Fed decisions suggest, then demand for short-dated instruments will also decline. The stock of debt assuredly will not decline, meaning future issuance plans is likely be forced to increase longer maturity issues more than if the ATI strategy had not been used and pushing up yields which until now may have been artificially constrained.

The new administration may enter office just as the Activist Treasury Issuance is forced into reversal, with unfortunate effects on the benchmark 10-year yield. Perhaps another reason for the post-election rise in yields.

Meyrick, you start from the standpoint that govt debt is a problem that needs solving. It isn't necessarily so. Federal govt debt might well be at 122% of GDP in 10years time, but how do you know that is 'too large' and therefore a problem? It might be 'too small', which will also be a problem that requires solving.

The Fed govt issues its currency, the USD, as a public good. Its debt IS its currency. It also sells bonds and bills as a public good. There's no fundamental reason why it has to exchange its issued currency for bonds, but it can do so, if the private sector prefers to hold its currency in fixed term savings accounts rather than am=n interest bearing checking account (a reserve account or a RRP at the Fed). Selling bonds is a service to the private sector. If the private sector doesn't want bonds......don't try to force them to buy them!

All the Fed govt should concentrate on is maintaining the value of the currency, by issuing just enough to meet demand (a little bit more if it wants to devalue the currency by 2% a year). If [everyone else in the World that isn't the Fed govt] wants to hold more USD, issue more. If it wants to hold those USD as a balance in a reserve account or RRP, issue reserves or expands the RRP facility. If it wants Bills, issue Bills, and if it wants 30yr Bonds, issue them. Do so 'in the public good'.

It is the value of the USD vs a basket of goods and services it is regularly employed to purchase that should be the main concern for the issuer of the USD, but as a proxy, its value against other major currencies is a useful yardstick. I'm not seeing many flashing warning lights in this respect. Has the Fed govt created too many of its USD or too few.......?

Meyrick, yes as your comment back implied to me. Greed and a capitalist system allowed to run amuck. Concur. Your description is much better stated in economics trained verbiage. Thank you.