Japanification of the entire non-US world

US asset demand amplified by Trump2

(of course Vietnam has a trade surplus, not deficit, with US, corrected now)

A few weeks have passed since the US election. With my wife Louise, I walk along the shore of the Lake of the Returned Sword in Hanoi. We are surrounded, like everywhere in Hanoi, by a swarm of mopeds. Neon lit skyscrapers provide the background. This place is absolutely jumping. But Vietnam has a trade surplus with the United States. A legend of this lake tells how the King of Dragons lends the leader of the Vietnamese people, Lê Lợi, a magic sword to defeat the Chinese. What will Mr Trump’s magic tariffs do, to the Chinese, the Vietnamese and to others, including Americans? Here is some partially-formed big picture conjecture that one outcome could be the Japanification of the entire non-US world underpinning the mother of all carry trades on US assets. It’s an outcome suggested by the immediate reaction to the election result. Will that last? That depends on how policy and reaction evolve. It been obvious for a while that for all the de-dollarisation claims of the last few years that the dollar has only gained in dominance. Maybe Trump2 provides the next logical step to overweening importance of dollar privilege, with all current imperfections magnified and exaggerated by pressing demographic and geopolitical pressures. If it’s a view that conflicts with previous outlines of the opportunities for global reset, I’ll happily acknowledge the dissonance. It is one path we need to consider. If it is wrong, some serious financial market adjustment is in order.

Trump2 tariffs aim to counter the imbalances in the world trading system. Yet, it is evident the Trump approach may well amplify existing imbalances, which exist for political and economic reasons that are probably impervious to American policy. The mess of policy and bluster flaunts USA as first choice destination of global investment. Trump has upped the price the rest of the world is willing to pay for the privilege of investment access. The response, so far, has been unambiguous. The world is willing to pay more, perhaps a good deal more. And the non-US world is prepared also to support higher American asset prices by lowering the cost of funding - devaluing against the dollar. We may be witnessing a move into a massive carry trade on US assets.

Since 5th November, the more outrageous the flaunting of institutional norms, on trade or on appointments, the stronger the US equity market, or the dollar and the higher the value of the dollar’s ‘exorbitant privilege’. The threat of tariffs has revealed the underlying demand demand for American financial assets, through bringing that demand forward. It has also revealed the low attraction of assets outside the USA - look at European equities. Indeed, one interpretation would suggest trade deficits are a prerequisite for foreign acquisition of American assets, so trade deficits ain’t gonna stop.

There are numerous signs of over-extension in financial markets. Key ratios of US equities are historically high: including Price/book, CAPE, Forward PE, EV/sales, EV/EBITDA. Leverage metrics show a financial system addicted to borrowing. There’s plenty of talk of a ‘coiled spring’ waiting to unwind abruptly.

Yet, current over-stretched valuations are underpinned by the very trade imbalances the Trump administration has promised to shrink. If Mr Trump truly wanted to reduce imbalances, he would threaten the basis for current financial market valuations. True reform would undermine dollar dominance, not demand a higher price. All signs currently point to a continuation of prior trends - see the bizarre threat to BRICS not to build a currency threat to the dollar, a possibility so remote as to be irrelevant but which would actually alleviate some of the unwanted side-effects of dollar dominance if it ever happened. Don’t look at what Trump claims to want, look at what riles him up. He wants more dollar dominance, not less, and with that goes more dollar demand. The higher demand means the spring is more tightly coiled. The old valuation metrics become less relevant - until some future reckoning breaks the illusion.

How radical the Trump shock has been so interpreted so far can be gauged by the interaction between the S&P500 and the dollar. Over a long history, the change in the value of the dollar shows inverse correlation to US equity performance. A stronger dollar is associated with weaker US equity markets. Currently, we have stronger equities and stronger dollar. Moreover, US equities are clearly outperforming foreign markets. The question of how much will the rest of the world pay is being answered. The global response to Trump2 is to award the dollar further dominance. Capital is desperate to deploy in the USA.

And a move to competitive devaluation against the dollar may have begun which would counter the impact of tariffs and further bolster capital flows into America. Consider the global monetary cycle, which accelerated since the US election result. An important gauge of the pressure to revalue the dollar (or devalue non-dollar currencies) came last week from the ECB’s Francois Villeroy de Galhau, governor of the Banque de France . He suggested the ECB should aim to reduce rates to neutral, and perhaps lower than neutral. “Should we go further...? I wouldn't exclude it in the future, if growth were to remain subdued and inflation at risk of falling below target.” This is an extraordinary admission of European economic weakness; an exact mirror of the bluster of American ascendency coming from across the Atlantic. One ECB member does not a policy make, but its a strong signal of likely direction. Capital has taken note.

Exactly how US equity valuations respond to widespread tariffs may depend on the interaction of the dollar and monetary policy both at home and abroad. Will the rest of the world confirm its bias for American assets?

If global monetary easing stimulates money creation more than the rise in the dollar the liquidity boost will provide additional support the S&P500 - as this is where a good part of excess liquidity will end up if existing capital channels are not addressed.

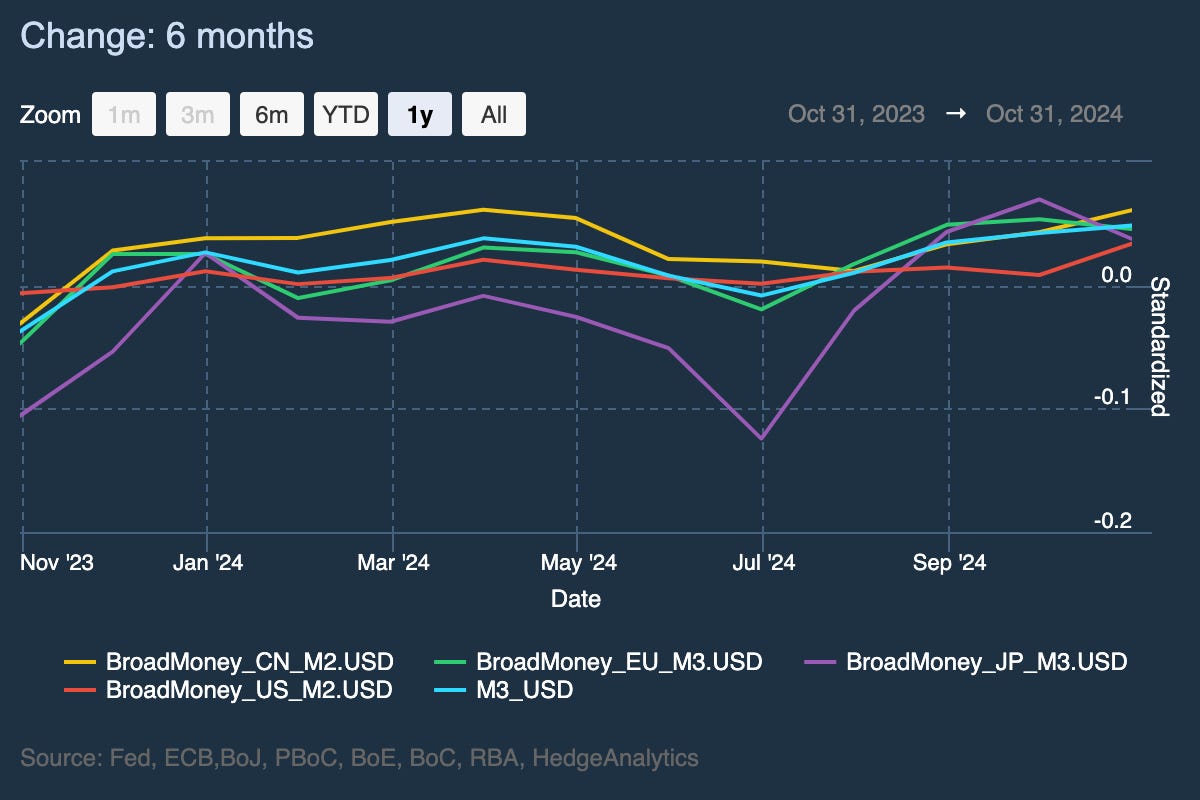

On recent trends, broad monetary aggregates globally have delivered more than enough stimulus in dollar terms to offset the rise in value of the dollar. The difference between dollar rise and money creation can be thought of as financial inflation, which find expression in biddnig for US assets. Yes, these trends precede the US election and will need to continue to sustain current elevated valuations. But non-US monetary authorities may not have an option if they wish to avoid a deflationary slump at home. This sets up a dynamic where prolonged funding can be provided by foreign investors into the US. What we may be witnessing is the Japanification of the entire non-US world, creating a global carry trade on US assets. History suggests such trends can last for decades.

What could change this? Well, capital controls of some sort would help adjustment. Again, this seems highly unlikely. Another source of adjustment may come in an abrupt return to peaceful co-existence - in Ukraine, Taiwan and the Middle East. That’s possible, but uncertain at best. It is also possible that raising the price of dollar dominance eventually and abruptly reveals the economic contraditions - perhaps in a conflict over foreign acquisition of American assets. Or maybe the rise in yields in an unreformed fiscal landscape abruptly curtails demand. That’s for the future to unfold.

For now, investors are showing concerted support for existing capital flows and even amplifying them. That’s great for Wall Street and certain exporters. It is no good for many others in America and the wider world.

Unless we're implying stocks are the next primary reserve asset then this doesn't apply to sovereigns - which is what matters when it coems to the topic of de-dollarization. In fact, de-dollarization involves the selling of USTs which will only exacerbate the strengthening of the dollar. So the problem for the US is not the dollar or demand for it's risk assets, but rather it's dwindling demand for it's largest export - US Treasuries which as Michael says essentially funds the country. Sovereigns now own 8T (US NII of -80%/GDP) of them as primary reserve assets and has been losing demand (from nations that produce) because of it's negative real returns, sanctions/account freezing, and ultimately the breaking of the US's petrodollar commitment with the globe since 2008 to keep the "dollar as good as gold". The game is over if nations continue to seek alternative "neutral" reserve assets and begin pricing commodities in non-USD currencies (which is also happening, net settled with not USTs, but gold). The strong dollar furthermore will accelerate this as foreign nations are short 13T of US denominated debt. When the dollar gets stronger, they will liquidate their net 22T of USD assets (8T of which are USTs) to manage their dollar needs. The only way for this to reverse is for Trump/Bessent to focus first on reducing the deficit and debt/GDP.

Of all the foreign investment into the US in the 12 months to end September 2024, the NET flows were as follows (according to the Treasury's TICS data released 18th November): +$1016 billion into fixed income securities, -$19 billion into US equities. Overwhelmingly, the fixed income inflows went to the US's Treasury Market, thus helping fund the $1.8 trillion bugdet deficit in Fiscal 2024 (also year to end September 2024). That deficit will be over 40% of all deficits worldwide: not bad for a country with 4.2% of the world's population.

Meanwhile the US is running a current account deficit of almost $1 trillion - 62% of all current account deficits worldwide. On the other side you have the rest of the world which by definition funds this deficit (since the US Dollar is broadly stable) with c62% of the world's NET mobile savings derived from their aggregate current account surpluses. But those savings are buying - AGAIN ON A NET BASIS - debt instruments (especially Treasuries) rather than equity instruments.

Am I the only one that thinks these stats jar with the prevailing Ra-Ra narrative? What am I missing?