Huge heap of dimes and bills

To stop the losses, Fed aims to restart its securities purchases programme

The Fed agrees with me. In the last post I claimed the “federal government is going to miss the profit transfers to the tune of hundreds of billions of dollars from the Fed for many years.” The Fed’s own projections suggest the U.S. Treasury will miss between US$160 - US$240 billion of expected remittances from the Fed from 2023 to 2026. But the big surprise is the Fed expects to limit that loss by returning to buying securities, funded by issuing a lot more dollar bills.

There are two papers ( here and here) that provide the Fed’s own assessment for the QE loss and ‘deferred asset’. Those papers provide an explanation for how large the losses on QE will be, how big the ‘deferred asset’ will be and how long it will remain on the balance sheet. Along the way we discover:

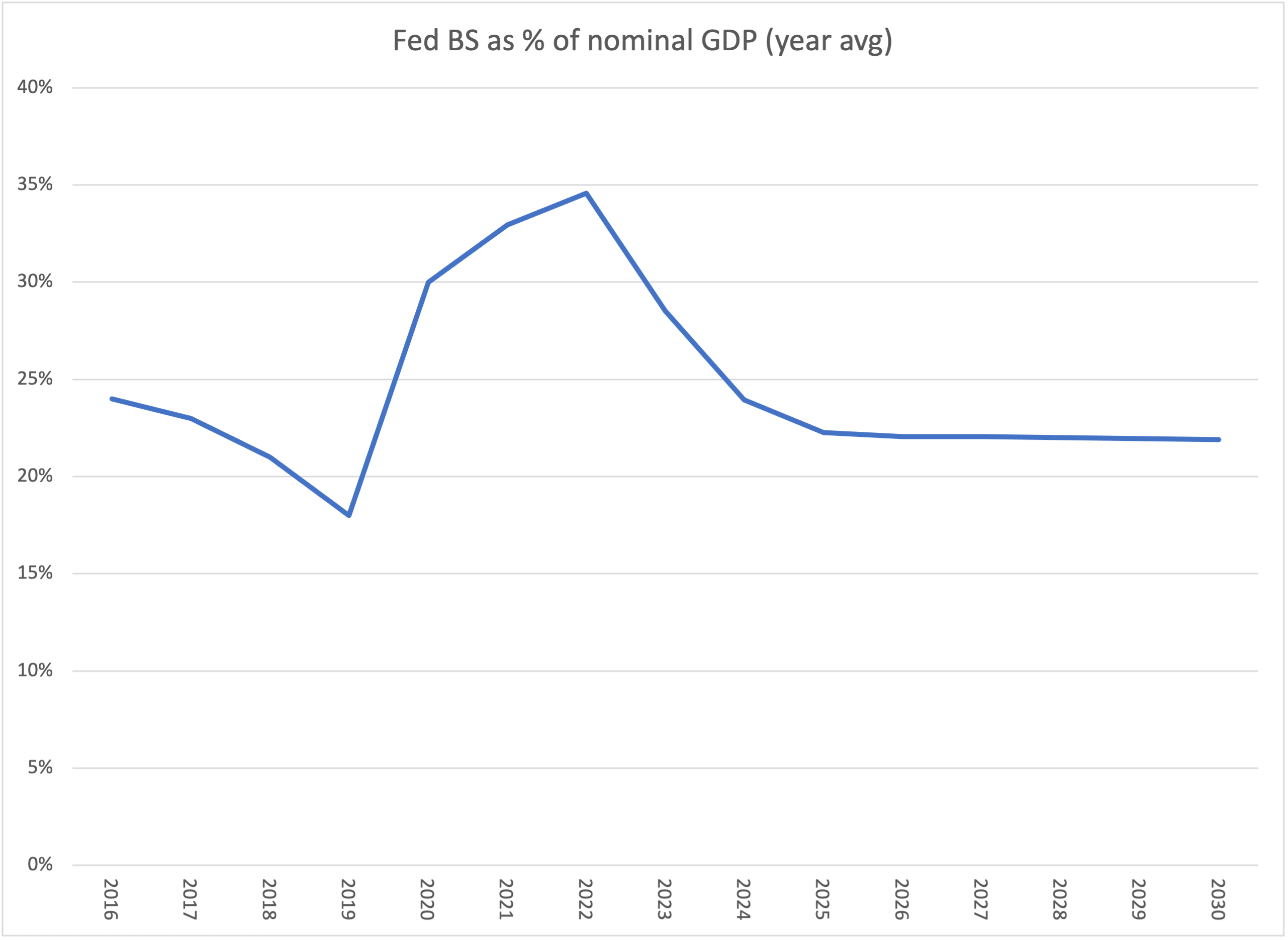

The Fed sees the balance sheet remaining huge for the foreseeable future, never less than 20% of GDP.

The continued massive size of the balance sheet is due to resumed buying of securities from 2026 onwards, with the securities portfolio growing at 4% per year.

The Fed seems to assume an inverted yield curve until at least 2030. Can commercial banks can live with that?

The ‘deferred asset’ (loss on QE) will peak at US$58bln in 2024 and will have eroded completely by 2026, leading to a resumption of remittances to the Treasury.

There is no sign of the Fed’s balance sheet returning to pre-GFC ‘normal’ size.

Obviously, the good news is the ‘deferred asset’ peaks at only US$58bln in 2024. The less good news is this exceeds normal capital of the Fed which is around US$50bln.

And their loss assumption is based on the Summary Economic Projections (SEP) released in June 2022. Since then the Fed has raised short-term interest rates above the level in those projections, and has more rate rises to come, so the Interest Expense on its portfolio of assets will be higher than expected, meaning the loss, at least in the short-term, will be higher than the baseline assumed in these papers. But rates might also fall sooner than expected, so we can’t be too picky.

My eyebrows rose a bit when I saw that the papers assume interest income rate remains below the interest expense rate till the end of the decade. The interest income divided by expected SOMA portfolio is expected to rise slowly to 2.8%, while interest cost divided by outstanding Reserves/RRP never falls below 3.2%. This despite claiming to using June 2022 SEP projections where medium-term Fed Funds rate falls back to 2.5%. Maybe I need some tutoring on these calculations.

How do I calculate the Treasury will miss US$160 - 240 billion till 2026? The average transfer from Fed to Treasury from 2016 till 2022 was US$80 bln per year, the lowest transfer was US$54bln in 2019. The Fed projects it will miss payments for 3 years, meaning the Treasury will miss between US$162-240 bln it had become used to receiving since 2016. Is that a false calculation? I guess it depends which department you ask to cut back its spending or which taxpayer you ask to make good the absent transfer from the Fed.

The big surprise in the paper was that to way the loss on QE is limited to ‘just’ US$58bln held in the ‘deferred asset’ is because the Fed is assumed to resume buying securities which pay a positive return, funded by currency (notes and coins) which pay zero interest, rather than reserves (which pay interest). Yes, this is seigniorage in action, but it does represent a huge increase in cash in circulation at a time when the Fed seeking to contain inflation.

Are “FEDS Notes” actual policy guidance or just some economists building models?

I wasn’t aware QT had a termination level or timeline. Much less aware that QE5 (or whatever number we’re on now) was a policy or market expectation.