Bad Habits Are Hard to Kick

More QE from major central banks is heaving into view

A question among friends arose this week: will the ECB or the Fed restart QE first? The ECB seems to face an epochal economic threat that may demand QE quicker than most suppose. Then there’s the Fed. The ‘new monetary framework’ that evolved since the GFC demands ‘ample reserves’ to keep the show on the road. The Fed may need QE (or some ‘facility’ which does the same thing) for technical plumbing reasons. For central banks, like all of us, bad habits are hard to kick. The race to QE could end in a tie.

The ECB Case for QE

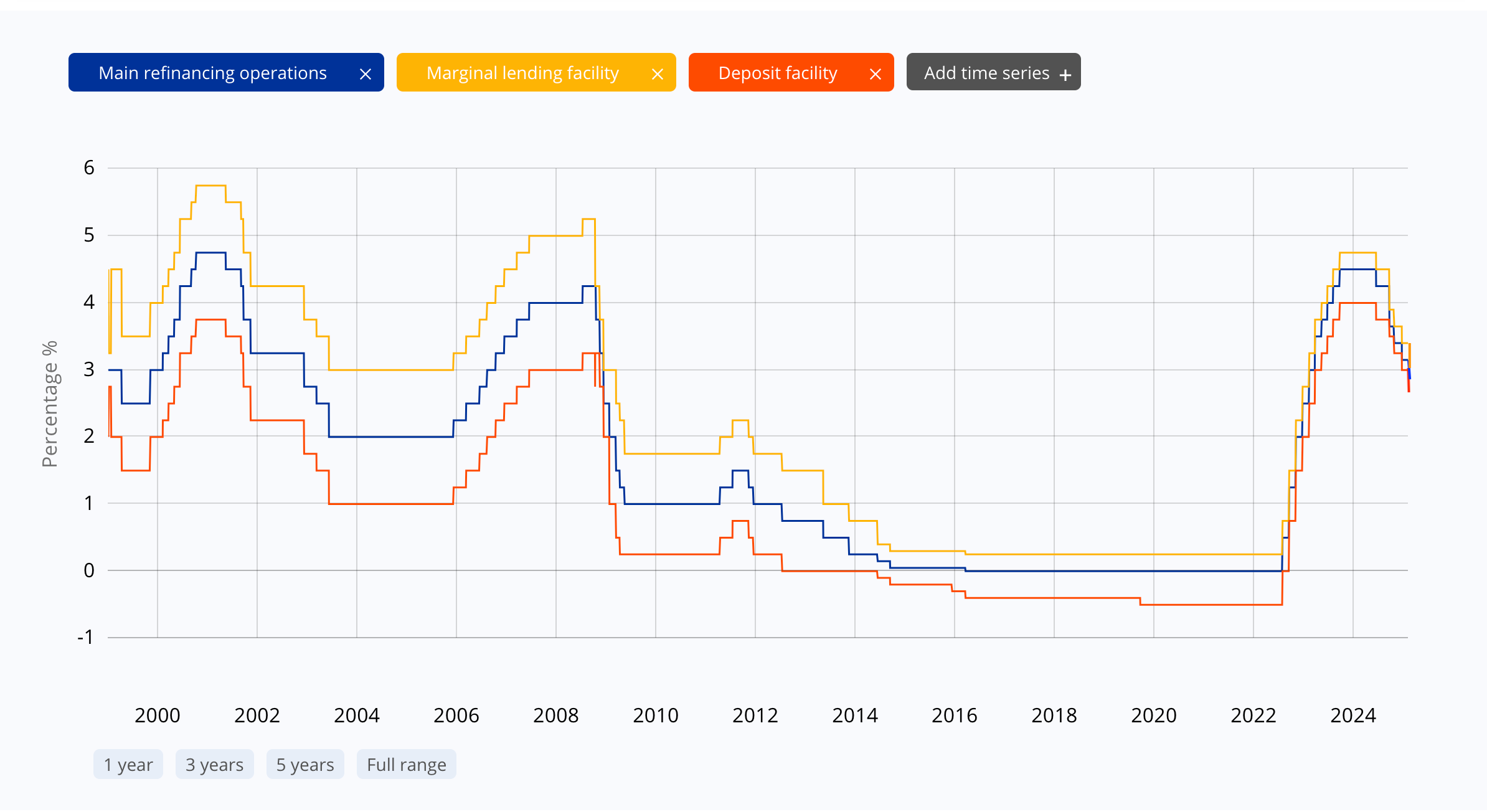

At last week’s monetary meeting the ECB reduced rates by 25bps to 2.75% on the deposit rate, 2.90% on the main refinancing rate - the lowest rates since early-2023. In their statement the ECB said “financing conditions continue to be tight… because our monetary policy remains restrictive.” So, more cuts to come. But the statement also restated “we are determined to ensure that inflation stabilises sustainably at our two per cent medium-term target.” It is a commitment that may pose a future dilemma given the parlous economic backdrop.

In 2005, the ECB estimated euro area trend potential growth to be in the order of 2-2.5% per annum. Twenty years later things look much worse. Their most recent estimate of potential growth rate is difficult to find, but can be approximated by projections for 2029 at 1.3%. This justifies president Lagarde’s claim that ‘our monetary policy remains restrictive’. The fall in potential growth of ~1% whilst maintaining more-or-less the same inflation target suggests interest rates should be set ~1% lower over the economic cycle. Yet current interest rates are set at almost exactly the average level of 2000-2008.

In fact, the long-term potential growth rate of the EuroArea, afflicted by elevated energy costs, geopolitical threats, legacy industrial capacity and demographic decline, may be closer to 0% than 1.3%. And even short-term prospects are poor against a backdrop of wars (both trade and actual hot wars!) - even acknowledging rising capacity for bank lending.

The EuroArea has a long-standing potential growth problem. Just look at the ever-widening gap in GDP/capita compared to the US. But circumstances since the Ukrainian invasion and China’s overt dominance of the global auto sector have radically undermined an already parlous economic equation in Europe.

The previously accepted solution combined cheap Russian energy with export prowess, together was immigration to offset demographic decline. None of those supportive elements remain unscathed. Energy has become permanently expensive, and may increase if the ill-advised commitment to Green Transition remains. High-end engineering dominance has collapsed since 2019. Immigration is no longer a palatable option to fix the demographic problem - witness the recent CDU/AFD putative alliance. Indeed, adjustment to pre-existing migration policies is likely to require additional (non-productive) spending.

The old European economic model is so comprehensively bust that the only viable long-term option may be the Japanese route - massive and sustained government spending backed by unconventional monetary policy. It is a policy that is hard to accept today because most are still digesting the large step change in price level. But it looks inevitable. And with the revised fiscal rules offering more leeway than before, there is room for the ECB to shoulder more of the burden of government issuance. Central banks are there to help in wartime - it was their original function.

This outlook places sustained downward pressure on the exchange rate. I fully expect parity to be achieved in the next 3-6 months. The move to parity is likely to be encouraged by the realisation that once again existence will trump price stability. Long-term fiscal pressures are almost certain to spread to Germany over time. From being a fiscal anchor for the credit of the entire bloc, Germany looks set to gravitate towards a debt/GDP of 85% by the mid-2030s, from 63% now - assuming it takes both its social and military commitments seriously. French fiscal stability is far from safe. Increased European defence spending backed by fiscal expansion might at least help raise the growth rate.

This all sounds a forecast for the long term. But the long-term has a habit of concatenating into the present for the EuroArea. It is entirely possible that running down of personal savings can generate short-term optimism. But the combination of likely tariffs, geopolitical costs, demographics and a unusable business model will bring forward the Japanification of Europe, opening the door to further QE. I’d give it a year.

The Fed Case for QE

Unlike the EuroArea, the United States economy powers ahead, at least for now. So why would QE loom for the Fed? It looms because of the post-GFC arrangement of monetary plumbing. We have returned to a pre-lapsian state of ‘required reserves’ for the banking system. The distinction from the old arrangement is that rather than the central bank demanding precautionary reserves, it is the commercial banks themselves who demand precautionary reserves.

Banks need reserves for two main purposes:

precautionary buffer against funding challenges

exchange medium for securities settlement

Unfortunately, the ‘ample reserves’ policy means the Fed has no reliable means of estimating that combined demand for these purposes - though the Fed pretends they do. If they get it wrong, as happened in September 2019, repo rates spike, positions get dislodged and the Fed is justifiably accused of losing control of monetary policy.

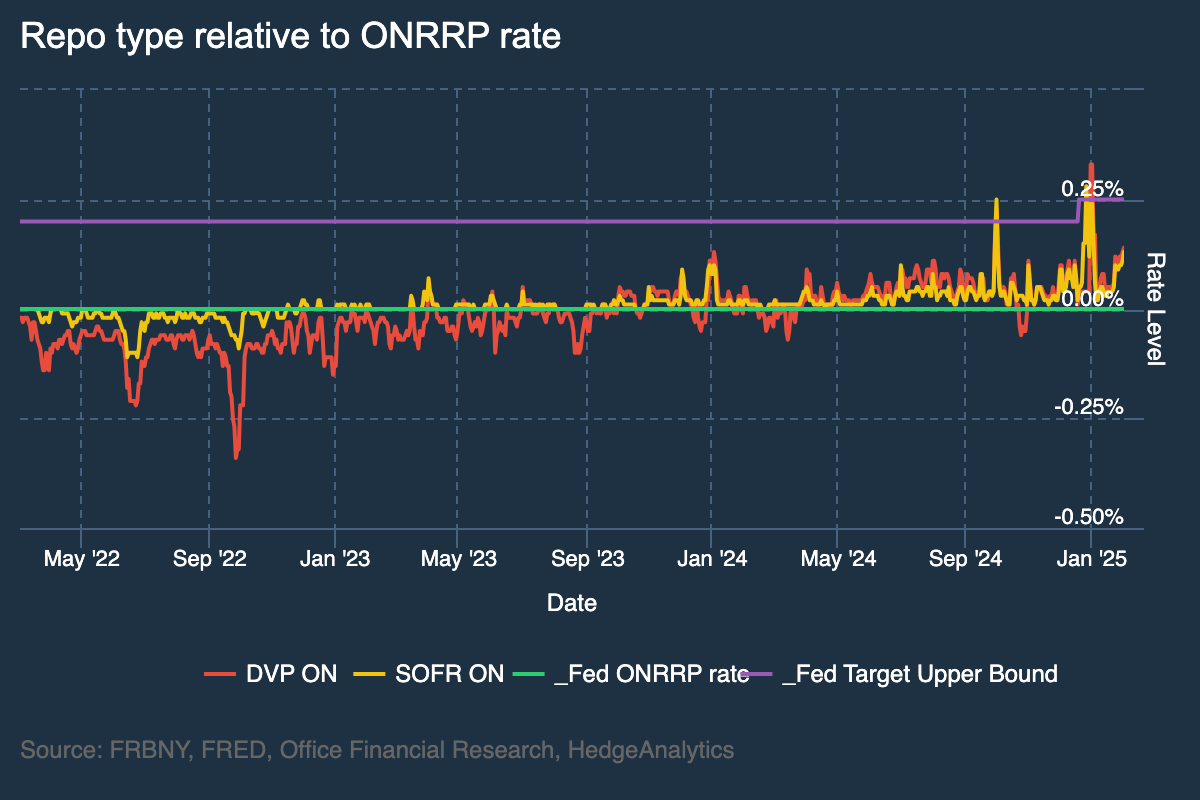

As it stands, the run-down in ONRRP holdings and the enforcement of debt ceiling restrictions place a growing strain on liquidity which has already shown up in recent quarter-end and year-end repo pressures, creating spikes well above the theoretical ceiling set by the Fed in the Standing Repurchase Facility.

Fed measures for reserve demand

The Fed measures current funding pressures by a measure called Reserve Demand Elasticity which assumes demand for reserves is linked to total assets in the banking system (not deposits). The choice of assets (not liabilities) and the choice of such a wide definition of assets should elicit some reflection on whether this is really the right measure to gauge funding pressures. The measure is not currently showing signs of stress, despite spikes in repo at both end-September and end-December.

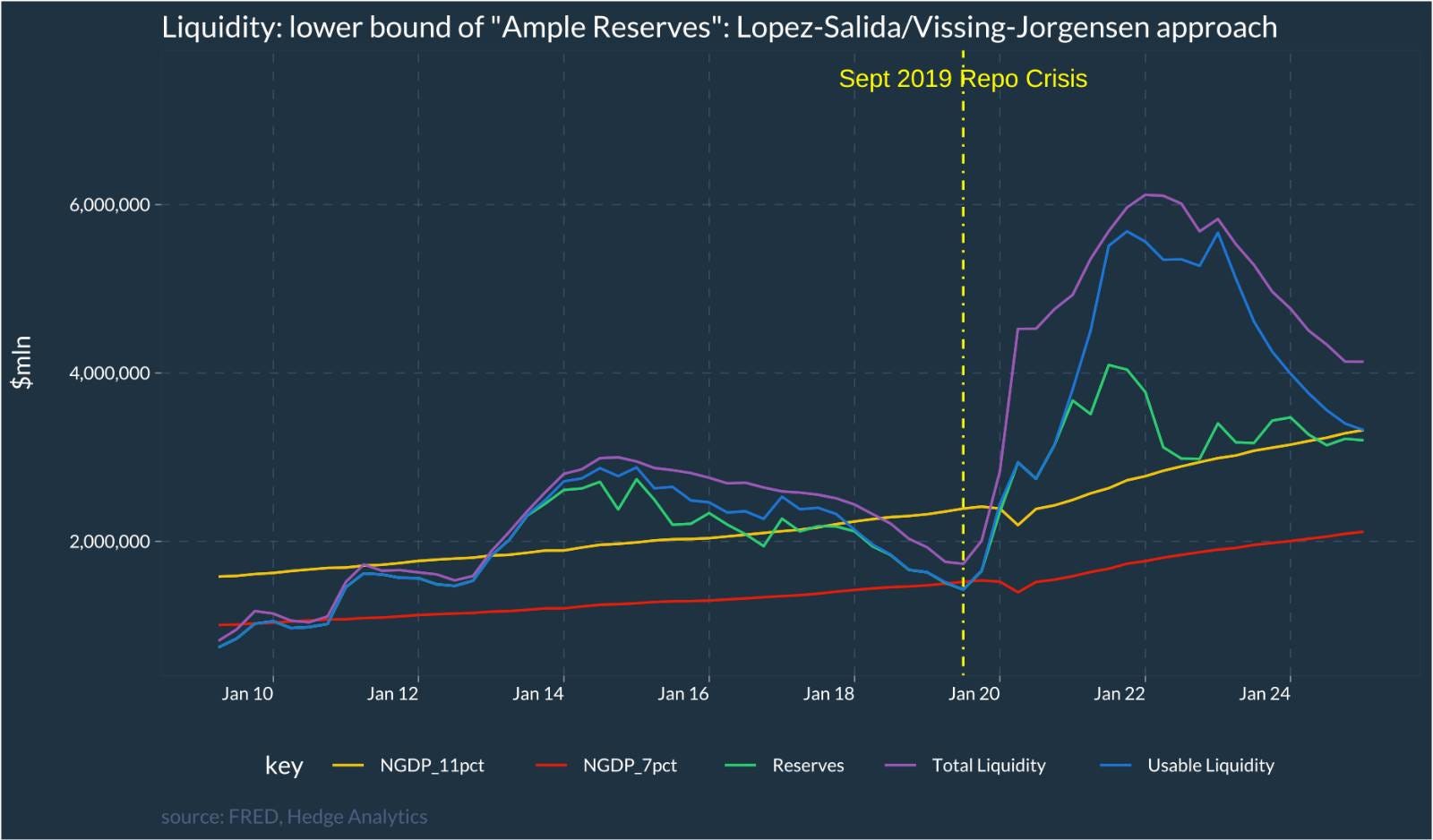

Another approach is taken by Lopez-Salido/Vissing-Jorgensen suggests deposits do play a role, which I have simplified into a measure of reserves/NGDP. That is unfairly prescriptive but has the benefit of being easier to display.

Both measures clearly identified possible trouble ex-post for September 2019. Neither suggest imminent funding issues in money-markets - though the Lopez-Salido/Vising-Jorgensen approach may indicate approaching caution.

That said, the system is constantly evolving. Reserves have plateaued at around $3.3 trillion, the ONRRP is depleted almost completely (holding $122 bln currently) and the other main source of liquidity (Treasury General Account) is unlikely to add to liquidity until the debt ceiling is lifted and even then it is likely to require a precautionary stock of approximately $600 billion (currently $811 billion). A sudden demand for liquidity could translate into a spike in rates.

One area in particular worth monitoring is the persistent rise in DVP repo, often used for funding cash/futures basis. Total daily turnover of DVP has risen to $2.3 trillion, and most of that is settled through FedWire Securities Service using reserves.

An additional $4.7 trillion per day is cleared through FedWire Funds Service, meaning reserve settlement through all Fedwire turns over $7.1 trillion per day, against an outstanding stock of reserves balances of $3.2 trillion. Velocity of greater than one is no problem for reserve settlement via FedWire - historically it was much higher. However, the reserves used probably need to be unencumbered. The Fed does not appear to know how much reserve velocity is acceptable to the banking system

None of this is 'catastrophic' - a workaround could be found in the short-term. If there was a spike in rates the Fed can expand the list of counterparts for the Standing Repurchase Facility, or come to some pass-through agreement. This would effectively disguise a return to QE as simply providing a short-term repo backstop. But QE it would be unless it really was temporary. The system that evolved post-GFC requires ample reserves to work, and we still don’t really know what ‘ample means'.

There is a very good chance some proto-QE appears in the United States within twelve months, possibly sooner. And for different reasons a similar fate awaits the EuroArea. Who will get to the QE gate first?

It just seems like QE never stopped. Does printing new money every week to cover your operating expenses count as on-going QE?

https://fred.stlouisfed.org/graph/?g=1Dp30

Yes agree this system cannot continue. It has run its course. We now have a system of Creditism, NOT capitalism. The games we have been playing since the 80's can no longer go forward. We lived off the fat of the land for 40 years or so and it is about over.

Hopefully Trump will set up this Sovereign Wealth fund properly (keep the money away from the politicians to buy votes with?). If he does, we can use it as a venture fund type set up to fund future technologies we need. Create good purposeful jobs, cure diseases, grow our way out of this mess of an economic system we now have. The bond market is a joke. When they crash the system, we the taxpayers pick up the bill as usual. We taxpayers will fund future growth and technologies, NOT the broken bond market. They have had their day, let's move on.

If we keep following the English system, we are doomed too. Remember, we are plutocrats, they are autocrats. Big difference. We can change, money there! yes, we'll do it. Aristocrats don't think that way. We need to leave the Brits and Europeans to their own devices, they usually do us no favors.