A tale of 2 QEs.

QE losses = increase in private wealth. The BoE provides a massive boost to private wealth. Arrangements need to be revisited.

When the central bank loses money on its QE portfolio, the resulting payment moves from the public sector (broadly defined) to the private sector. This boosts private sector wealth. It may also impact growth and asset prices. The central bank can lose money through the payment of interest on reserves and/or through outright losses on the bonds bought by QE. We look at the example of the Federal Reserve and the Bank of England - we would love to look at the ECB too, but they do not provide sufficient data.

The comparison is stark, and deeply unfavourable to UK official sector which is paying way more than the Fed relative to the size of the economy. At a time when the UK fiscal position is a point of focus for Gilt investors, it makes sense to revisit

the payment of reserves and

the Indemnity of Bank of England losses by the Treasury.

It is even possible to retain the Indemnity but book the losses as a derivative held by Treasury (liability) and the Bank of England (asset). This is an arrangement instituted by the Bank of Canada and the Reserve Bank of New Zealand. This is something I advocated with my friend Chris Marsh in our submission to the UK’s Treasury Select Committee. It needs further discussion.

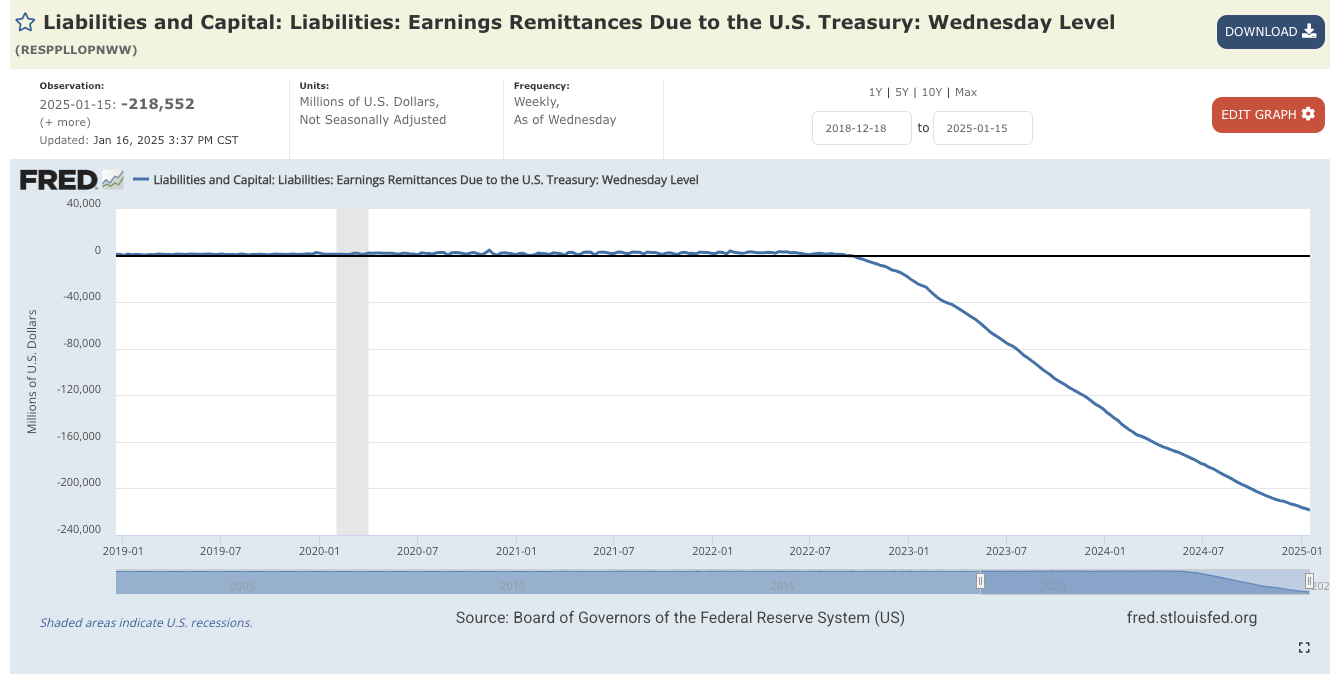

The annual loss recorded in 2024 on the QE portfolio of the Federal Reserve (face value loss plus net interest loss) amounted to US$87.2 bln dollars, with the total cumulative loss standing at US$218.5 bln. At the end of 2024, the annual loss recorded in 2024 on the APF portfolio of the Bank of England (face value and sales loss plus net interest loss) amounted to approximately GBP40 bln.

At end-2024, the US economy had a nominal GDP of approximately US$28.5 trillion whereas the UK economy had a nominal GDP of approximately GBP2.8 trillion, making the US economy about eight times the size of the United Kingdom. Comparing the relative boost in 2024 to the non-government sector from central bank losses shows the economic boost provided by the Bank of England is massively bigger (+1.4% of GDP) than that provided by the Federal Reserve (+0.3% of GDP). That is not chicken feed.

It is very difficult to determine how payments from Fed to the private sector will evolve in 2025 or later. Some time ago the Fed predicted the peak loss would occur at end-2024, though those predictions were presumably made under much lower interest rate assumptions.

In contrast, the Bank of England provides regular updates (in picture form) of how it estimates the losses will evolve. According to the latest Bank of England report from Q3 (published in November 2024), the losses for 2025 are expected to amount to GBP23 bln.

In comparison, here is the cumulative loss recorded by the Fed, couched as remittances foregone to the Treasury.

If we consider the central bank losses as a monetary or fiscal transfer to the wider economy, then the comparison between the US and UK is stark.

First off, let’s look at 2024.

Adjusted for the size of the economy, the scale of Bank of England losses paid to the non-government sector in 2024 is 4.5 times larger than that of the Fed.

The payments of both central banks mean the consolidated government balance sheet is poorer and the non-government sector balance sheet is richer. The non-government beneficiaries include corporates (including banks), households and foreigners.

There is a wealth impact question and an accounting question to answer.

The wealth impact is cloudy. How do the newly richer groups receiving payment from the central bank react to the transfer? The answer is not clear. Perhaps they simply account for their higher balances and do not adjust their spending patterns. However, the bigger the transfer, the more likely the increase will lead to increased consumption, or increased investment - just as with any fiscal/monetary boost.

It is frankly unlikely that the boost of 1.4% of GDP provided by the Bank of England (mostly to the banking sector) has not had any impact on asset prices or economic activity. Yet growth in the UK is anaemic and asset prices have underperformed. That is shocking.

It is likely 2024 provided the largest such transfer by the Bank of England. But compared to the Fed, very large transfers will continue for several years according to the Bank’s own forecasts.

As Treasury and Gilts prices have fallen recently, the eventual costs may exceed projections of both Fed and Bank of England. The forecasts are especially sensitive to short-term interest rates. In the last 3 months expected rate cuts have been considerably reduced meaning losses may remain for longer than anticipated. There may be higher than expected transfers from both central banks to come. The largest upward revision is likely to come from the Fed, though we don’t have any up-to-date research to judge this by.

The accounting question is more important. And here too there are large differences between the Fed and the Bank of England.

The Bank of England QE programme (known as the Asset Purchase Facility) was indemnified by the government since 2009. The Indemnity means losses are funded by the Treasury through bond issuance.

This is not true of the Federal Reserve, which books the losses as a ‘deferred asset’ and simply issues reserves to the banking system to cover the losses until such time as seigniorage profits cover the loss. That means the Fed acquires a liability (aka a ‘deferred asset’), but the Treasury does not have to issue bonds to cover the loss.

The Bank of England arrangement therefore adds to measured government debt while the Federal Reserve arrangement does not.

This is a ridiculous arrangement for the Bank of England. If the losses are so large, relative to the size of the economy, then it makes sense to mitigate the impact on government finances. Instead, the chosen arrangement falls directly onto the UK finances.

At a time when the UK fiscal position is a point of focus for Gilt investors, it makes sense to revisit a) the payment of reserves and the Indemnity of Bank of England losses by the Treasury. It would be possible to retain the Indemnity but book the losses as a derivative held by Treasury (liability) and the Bank of England (asset). This is an arrangement instituted by the Bank of Canada and the Reserve Bank of New Zealand.

Keep reading with a 7-day free trial

Subscribe to ExorbitantPrivilege to keep reading this post and get 7 days of free access to the full post archives.