Carl Jung: “a kind of mask, designed on the one hand to make a definite impression upon others, and, on the other, to conceal…”

In psychology, as the quote above suggests, masking is the process of hiding reality to avoid psychic harm. Masking may be intentional but is often unintentional. Usually, the term applies to an individual’s response to trauma, or difficulty in processing social pressures. Is the S&P500 exhibiting similar traits? Here are a couple of thoughts.

Geopolitics has been deeply unsettled since early 2022. Trade blocs are realigning, or talking of realigning. Over quite a short period, established supply chains have been challenged. In response ‘friend-shoring’ became a major policy goal. The Biden administration initiated ‘Trusted Digital Ecosystems’ in the fall of 2022, and there are signs of progress. 2022 not only marked the 200th anniversary of diplomatic relations between Mexico and the United States; it was also the year when Mexico clearly overtook China in total trade with the US; surely a victory for ‘friend-shoring’. The Mexican trade out-performance has continued into 2023.

Secretary of the Treasury Janet L. Yellen outlined ‘friend-shoring’ in a semi-official manner at the Atlantic Council, April 13, 2022:

“Let’s build on and deepen economic integration and the efficiencies it brings—on terms that work better for American workers. And let’s do it with the countries we know we can count on. Favoring the “friend-shoring” of supply chains to a large number of trusted countries, so we can continue to securely extend market access, will lower the risks to our economy, as well as to our trusted trade partners.”

In response, the Mexican peso has been among the best performing currencies in the last twelve months - though we shouldn’t forget the improvement in bilateral relations under the current administration.

The big test is whether ‘friend-shoring’ actually will ‘lower the risks to our economy’, and that test hasn’t happened yet. A degree of scepticism is warranted about just how much can be achieved in a few months, or years; especially as China may have diverted trade with the United States through countries like Mexico. China may be masking its true export numbers.

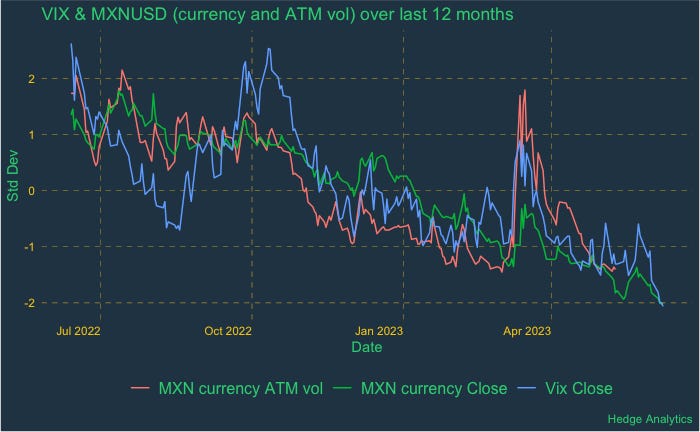

So, its worth keeping an eye on another relationship; the big increase in correlation between the Mexican currency, the cost of option protection on the currency and the VIX Index. All three measures, when normalised to a common unit (standard deviations) show remarkable co-movement over the last 12 months.

If the VIX index is indeed, the ‘Fear Index’ then there isn’t much fear about at present. There has been some backward and forward discussion about the very low levels of the VIX, especially as the breadth of the S&P500 market is incredibly narrow. It is partly offset by the relative increase in the skew in S&P500 options. Skew represents the relative price of out-the-money puts options compared to call options and recently reached its highest level for two years, even as (or perhaps, because) the VIX continued to decline.

The relationship between the VIX and the peso also may reflect a year of ‘friend-shoring’.

‘Friend-shoring’, per Yellen, has been sold as way to continue accessing international markets and supply chains while reducing geopolitical risks. But ‘friend-shoring’ cannot reduce geopolitical risks. There are coherent arguments that consciously impeding trade will add to the tensions between rivals. And the policy concentrates risks among the ‘friends’. In psychological terms there seems to be some kind of ‘masking’ taking place - equity markets camouflage reality to conform to pressures of performance, perhaps. ‘Friend-shoring’ may indeed be off to a good start between Mexico and the United States. But behind the mask the big threats continue. In Mexico masks are worn to celebrate the ‘Day of the Dead’, a celebration of dead relations. Let’s hope the VIX is not driven by a similar motivation.