A bit more of the same

A longer piece on ECB's move to 'improve the efficiency of monetary policy'

After yesterday’s post I had a few requests for further explanation. Why was yesterday’s ECB announcement ‘disingenuous? Is it important? Will it be important? Here’s an expanded response of informed guesswork. Happy to be corrected.

When a central bank releases a statement after a monetary policy meeting, we assume that all information in that statement is intended to convey something of consequence. Yesterday’s statement was divided into two parts. The first part outlined the decision to raise interest rates and the reasons for that decision. It also explained that future decisions would be guided by the determination to achieve the 2% inflation target. That information is clearly consequential.

The second part of the statement outlined changes to the remuneration of minimum reserves and made some specific claims I found unconvincing. This second part was itself divided in two. Part 1 claimed “this decision will preserve the effectiveness of monetary policy by maintaining the current degree of control over the monetary policy stance and ensuring the full pass-through of the interest rate decisions to money markets.”

No problem with that. In a floating currency, a central bank’s primary policy tool is either the supply of liquidity, or its cost. In a situation where system reserves are ample, supply of liquidity is not (generally) an issue and cost of liquidity is the primary consideration. The ECB would not be able to use interest rates to tighten monetary conditions if it was unable to control the cost of funds. And the essential support for money market interest rates in a system of ample reserves comes from the average interest rate paid on all reserves.

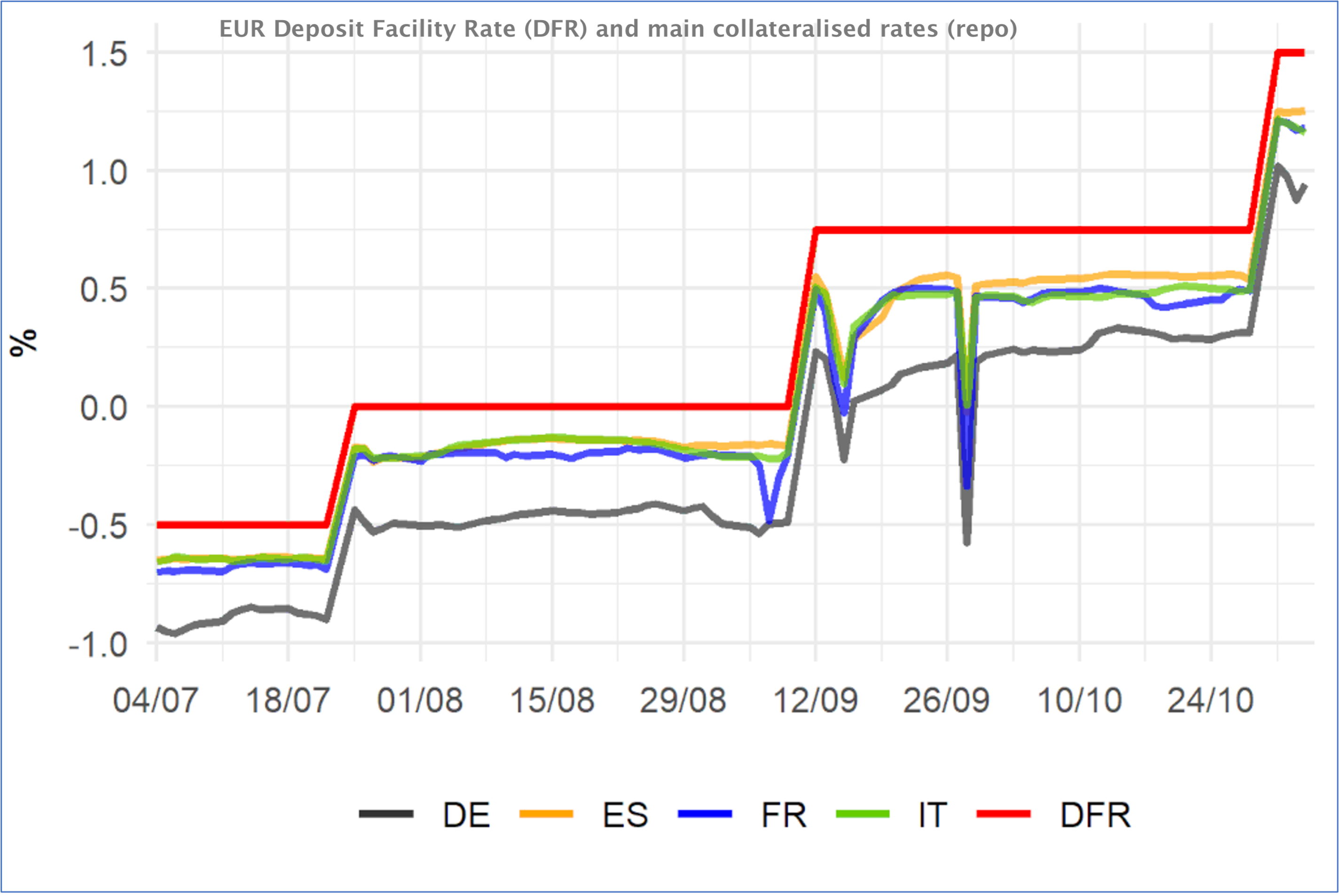

The EUR Short Term Rate (€STR) is the benchmark money market rate and replacement of EONIA. For years the €STR traded below the Deposit Rate, which is nominally the floor for interest rates in the Eurozone. Limiting the spread is important for continued confidence in the effectiveness of ECB policy.

Ample liquidity means banks need to be compensated to take on uncollateralised deposits, which places downward pressure on rates. The wholesale collateralised market (repo) has also traded below the Deposit rate due to scarcity of collateral, particularly for highest quality assets like German government bonds. Collectively these effects are because a/ central bank purchases (QE) depress rates through ample reserves and b/ regulations restrict bank balance sheet and attach premium to High Quality Liquid Assets (HQLA).

By ‘tiering’ the remuneration on reserves, will the ECB create an incentive for banks to close the gap between €STR and Deposit rate? That is not immediately obvious.

There is a recent precedent for a ‘tiering’ of reserve interest rates at the Swiss National Bank which was deemed successful in closing the gap between target and money market rate. Whether SNB policy is a template for ECB policy is doubtful.

The point of the SNB policy change was to encourage circulation of reserves from banks whose reserves exceeded a ‘threshold’ (paying 0%) to those whose reserves were less than the threshold - so with room to gain more interest on reserves from the central bank. The price at which reserves moved naturally raised the money market rate towards the target rate. The following slide is taken from the SNB presentation.

Superficially, the ECB seems to be attempting a similar ‘tiering’ of reserves. But there’s one key difference; in the ECB’s case required reserves will be remunerated at 0%, whereas the SNB remunerates required reserves at the target rate. This suggests Eurozone banks have an incentive to hoard reserves above required threshold, rather than ‘sell’ them to other banks. That’s odd.

If ECB ‘tiering’ is not aimed at narrowing the €STR and Deposit rate spread, then it is probably just a disguised bank levy. At current interest rates and required reserves, the ECB decision to pay 0% on required reserves will reduce commercial bank income by EUR 5.75 billion over a full year. That’s just over 4% of total profit reported by Euro-zone banks in 2022.

What is clear is that with EUR 3.6 trillion in overall ‘excess reserves’ mostly in the Deposit Account, interest on reserves will remain a very considerable drain on the profitability of the ECB and its members for a long time. So perhaps the modest reduction in interest payment the new policy represents is an attempt a deflecting criticism. If so, it is not an impressive gesture.

Part 2 of the remuneration section stated: “it (remuneration of required reserves at 0%) will improve the efficiency of monetary policy by reducing the overall amount of interest that needs to be paid on reserves in order to implement the appropriate stance.” My beef with this sentence is that overall, yesterday’s decision increased, rather than reduced, the cost of interest that needs to be paid on reserves. Yes, interest on required reserves was reduced, but the statement said ‘overall’ interest payments will be reduced. That is not correct. And in a central bank statement, accuracy is important. This is the ECB’s disingenuity.